The AI Blind Spot Lemonade, Chubb (and most insurers) Share

Dispatches from the Agentic Frontier is a new regular intelligence briefing for leaders in knowledge-intensive sectors. Each dispatch translates evidence from the frontier of agentic AI — practitioner experience, investor signals, strategy research, market events — into what it means for enterprise leaders building for competitive advantage. Some dispatches are field reports from practitioners who are 12–18 months ahead. Others synthesise emerging research. All are filtered through the Intelligence Capital framework developed in The AI Your Competitors Can’t Buy.

Today we provide a deep-dive analysis on Chubb and Lemonade - an insurance behemoth and an AI-native insurtech challenger - to elicit lessons for leaders across any sector.

Introduction

The CEO of Lemonade recently published an investor letter called ‘Why Incumbents Won’t Catch Up’ that has been circulating widely in insurance and insurtech circles. His central argument: that AI-native challengers like Lemonade have built a structural advantage that incumbent insurers cannot close — regardless of how much they invest in technology. It deserves a serious response — not a defensive one.

His core analytical framework is sound. His three diagnostic metrics are a genuine contribution. And his compounding physics argument is, structurally, correct.

But the piece contains one argument that needs a more precise mechanism, and one critical silence that his investors should be pressing him on. Most importantly, a remarkable coincidence of timing gives us a third data point that his binary framework — adapt magically or be disrupted — entirely fails to accommodate.

I want to address all three, because together they point toward something more strategically useful than either the challenger's narrative or the incumbent's defensive dismissal.

What Schreiber Gets Right

The Physics Is Real — And It Is Not About Technology

Let’s start with what is analytically sound, because there is a great deal of it.

Schreiber opens with a concept from the psychologist Daniel Kahneman: WYSIATI — "What You See Is All There Is." Applied to competitive threat assessment, the insight is this: incumbent leaders evaluate threats against what is visible — capital strength, distribution scale, brand recognition. They systematically discount the less visible architecture that actually determined the last round of market leadership changes.

The way Amazon's recommendation engine got smarter with every purchase. The way Netflix's culture moved ten times faster than Blockbuster's. The way new entrants aligned every incentive around the customer while incumbents aligned every incentive around the channel. You see the balance sheet and the brand. You don't see the compounding data loop and the cultural clock speed that will make them irrelevant. Schreiber is right that this cognitive bias explains more about the history of disruption than most boardroom conversations acknowledge.

His three diagnostic KPIs are also a real contribution.

The Scaling Quotient — how fast a company grows its customer base relative to how fast it hires — tests whether AI is genuinely replacing human effort or merely augmenting it. The Loss Adjustment Expense ratio — the cost of administering claims as a proportion of premium — tests whether the machine is getting more efficient over time. And what Schreiber calls Structural Precision — the combined improvement in profit per unit of risk and profit per pound of acquisition spend — tests whether the system is getting smarter, not just faster.

These metrics are observable, falsifiable, and considerably harder to game than NPS scores or deployment announcements. Any insurer that has not run these numbers on their own organisation, before an activist investor or a competitor's IR team does it for them, is leaving a strategic vulnerability unaddressed.

Most importantly, the compounding physics argument is correct. If two organisations invest in AI capability at the same rate but one began earlier, the gap between them does not shrink over time — it grows. This is the mechanism that underpins what I call Intelligence Capital — the institutional knowledge an organisation accumulates through every decision its AI systems deliberate on, which persists independently of the individuals who generated it and compounds in value over time, making it irreproducible by any competitor who starts later.

Schreiber arrives at this conclusion from the attacker's position. My own framework arrives at the same place from the incumbent's. Both arguments depend on the same underlying mechanism being true — and it is.

Schreiber is describing the Parity Problem — the condition where AI automation investment creates equivalence rather than advantage — from inside the disruptor. Every efficiency gain that incumbents call 'AI transformation' is exactly the kind of replicable, commoditisable investment his KPIs are designed to expose.

Where the Analysis Needs Qualification

Scope: Where This Argument Applies and Where It Doesn't

Schreiber writes from inside personal lines insurance. His named competitors throughout the piece are State Farm, GEICO, Allstate, and Progressive. His own products are renters, homeowners, and pet insurance — standardised, high-volume, low-judgment lines where algorithmic processing is most tractable, data patterns are relatively stable, and the primary underwriting question is amenable to statistical segmentation.

Within that market, his argument is coherent and his KPIs are relevant.

But his title — "Why Incumbents Won't Catch Up" — will be read by underwriters, COOs, and strategy teams across the full spectrum of insurance, including markets where his structural conditions simply do not hold. That generalisation is worth examining carefully.

In specialty commercial insurance, Lloyd's syndicates, complex casualty, and reinsurance, underwriting judgment cannot be fully systematised. A £50m Directors and Officers policy covering a company entering a new market, a complex marine cargo placement spanning six jurisdictions, a political risk programme in an emerging economy — these require synthesis of qualitative signals, market intelligence, relationship context, and professional judgment that no algorithm yet replicates reliably.

The broker relationships that bring these risks to market took decades to build and are not transferable. Capital market access creates real barriers to entry that a cloud-native architecture cannot dissolve. The product complexity is not a legacy inefficiency waiting to be engineered away. It is the product.

An insurer in specialty lines reading Schreiber's piece and concluding that their position is as threatened as State Farm's would be drawing the wrong inference. Equally, they would be wrong to conclude they are immune. The competitive dynamics are different. The timescales are different. And the form that AI advantage takes — which we will come to — is different.

Admiral Group — a 30-year-old FTSE 100 personal lines insurer operating in exactly the market Schreiber describes — offers a recent example of a third path his binary doesn't account for. In February 2026, Admiral acquired Flock, a digital fleet insurer built on proprietary AI risk models trained on hundreds of millions of miles of real-world driving data, valuing the insurtech at £80m. Admiral did not attempt to build this capability internally from scratch, nor was it disrupted by it. It partnered with Flock through Admiral Pioneer — its venture arm — then acquired it when the capability was proven.

This is what Schreiber's binary misses even within his own market: the mammal acquiring the mammal. A structurally protected venture entity, insulated from the organisational immune system, acquires specific AI-native capability for a defined segment. That is not a Triceratops failing to evolve. That is disciplined strategic portfolio construction. It is available to every well-capitalised incumbent who chooses it — in personal lines and beyond.

The Capability Layer His Compounding Argument Requires — But Doesn't Describe

This is where the analysis requires the most careful attention, because it is where Schreiber's compounding argument — which is correct in form — is applied to the wrong capability layer.

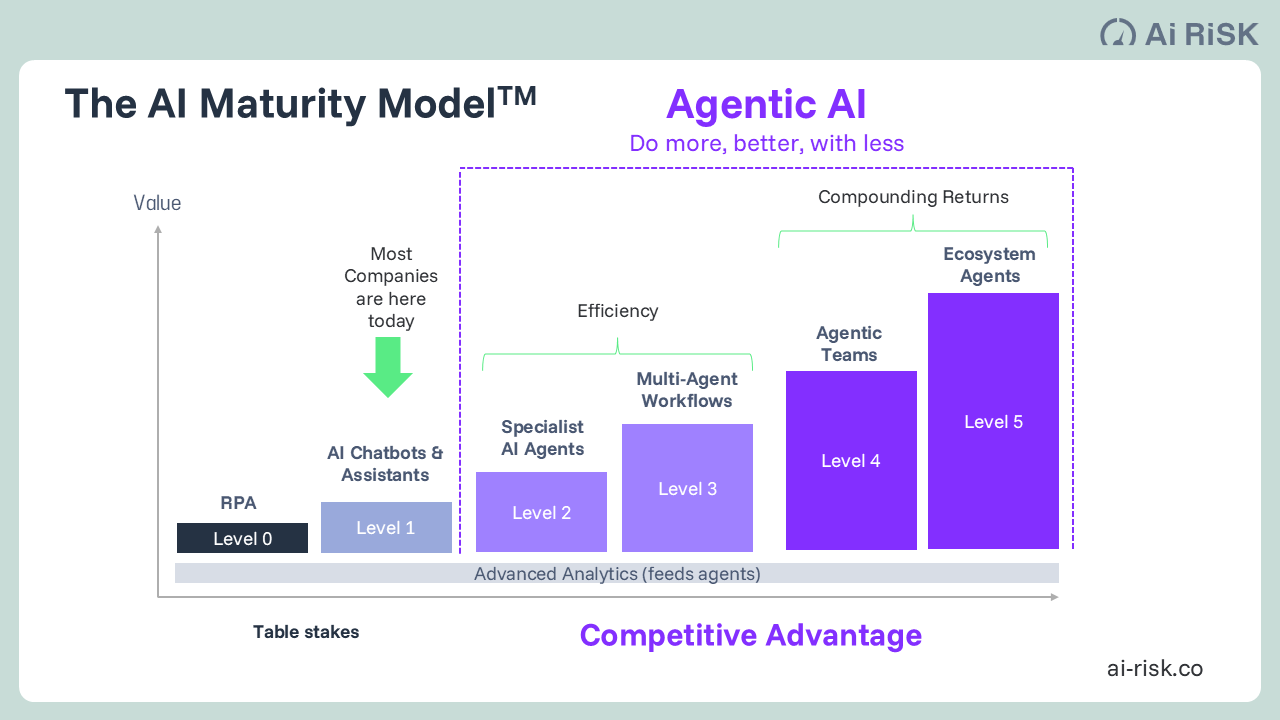

To understand why, it helps to have a simple map of AI capability. Think of it as a ladder. At the bottom — Levels 1 through 3 in the diagram above — sits everything from basic automation and chatbots through to sophisticated multi-agent workflows that coordinate tasks across a process end to end: document extraction, submission triage, claims routing, cycle time compression.

These are genuinely valuable. They are also, by definition, available to anyone willing to buy the platform that enables them. At Level 4 and above, something qualitatively different happens: AI systems stop executing and start deliberating — reasoning through complex problems, capturing that reasoning transparently, and building institutional memory that accumulates over time.

Lemonade's claimed structural advantage rests on three metrics: LAE compression, scaling without proportional headcount growth, and improving economic precision. These are valuable and genuinely impressive for a company of Lemonade's scale. They are also Level 1 through 3 capabilities: intelligent intake, automated workflow processing, algorithmic claims handling.

A competitor who deploys the same workflow automation platform in eighteen months achieves a comparable LAE ratio within two to three years. BCG research across hundreds of public companies found no consistent correlation between AI automation investment and sustained profitability improvement. The sectors investing most heavily in AI efficiency saw margins stagnate or fall. The efficiency gets competed to zero.

The genuine compounding asset — the one that cannot be replicated by purchasing the same technology at a later date — is not automated claims processing.

It is what happens at Level 4: deliberative agentic teams that capture structured reasoning with every decision, build institutional memory that compounds across thousands of cases, and encode expert judgment that persists independently of the individuals who generated it. This is Intelligence Capital. The question Lemonade's investors should be asking is whether their architecture has built this — or whether it has built a more efficient version of what every insurer will have by 2027.

The Critical Silence

Schreiber's three KPIs are chosen, whether consciously or not, because Lemonade wins on them. They measure administrative efficiency and scaling leverage. They say nothing about whether the business is pricing risk correctly.

A company with a 6% LAE ratio and a combined ratio consistently above 100% — meaning it pays out more in claims and expenses than it collects in premiums — is an efficient bureaucracy that destroys capital on every policy it writes. After a decade in operation, Lemonade has not demonstrated sustained underwriting profitability. The LAE metric measures the cost of processing claims, not the quality of the claims decisions themselves. An architecture that automates the processing of incorrectly priced risks faster is not building competitive advantage. It is building a more efficient path to capital destruction.

This is not a verdict on Lemonade's future. It is a demand for analytical precision. If the compounding architecture is genuinely generating institutional underwriting intelligence — better risk selection, tighter segmentation, improving loss ratios as the model learns — then the profitability gap is a strategic growth investment and the thesis holds.

If it is not, then Lemonade's claimed moat faces the same Parity Problem it is warning incumbents about.

The View from the Incumbent's Corner Office

Chubb and the Parity Problem

In December 2025, Chubb — a $56bn-premium global insurer and the highest-margin P&C insurer among the world's largest, at 16.4% operating margin against a peer group average of roughly 9% — published its investor presentation. Read alongside Schreiber's piece, the Digital Transformation section is analytically revealing.

Chubb has committed to automating 85% of major underwriting and claims processes within three years. It has 3,500 engineers already deployed. It is targeting a 20% headcount reduction and 1.5 combined ratio points of expense improvement through digital enablement. The presentation describes intelligent intake, no-touch processing, submission automation, and cycle time compression across every major business line.

Schreiber's Triceratops is moving. Fast.

But read the Chubb commitment carefully. Every capability described — automated intake, no-touch routing, AI-assisted recommendations, cycle time reduction — maps precisely to Levels 1 through 3 on our capability ladder. It is efficiency. It is genuinely impressive at this scale. And Chubb's own language reveals exactly where this trajectory leads: the presentation notes that "AI adoption is expected to surge and drive change across the industry" within the next two to three years.

When every insurer has deployed the same automation stack — and Chubb's own framing predicts that they will — what Chubb calls a competitive advantage will be what the BCG research already measured: a race to parity.

Lemonade and Chubb are, from opposite starting positions, converging on the same strategic destination. Neither has described what lies beyond it. That gap is where Intelligence Capital lives.

The Third Path

What Neither Narrative Captures

The binary Schreiber presents — be born digital or be disrupted — ignores the viable strategic path that the Admiral/Flock acquisition represents and that the most analytically honest incumbents are already executing.

The path is not "become Lemonade." It is not available and it is not necessary. The path is to build the compounding capability layer that neither Lemonade nor Chubb has demonstrably built — the Level 4 deliberative intelligence layer, where AI systems reason, deliberate, and build institutional memory rather than simply execute tasks — using the existing organisation's most durable competitive assets as the raw material.

Those assets are real and they are not replicable. Decades of complex risk decisions. Proprietary claims history across market cycles. Broker relationships built on consistent underwriting judgment. The expertise of senior underwriters and claims managers who have navigated hard and soft markets, and who will retire taking irreplaceable institutional knowledge with them unless the architecture is built to capture it.

Level 4 agentic systems — teams of specialised AI agents that deliberate on complex decisions, capture its reasoning transparently, and build institutional memory that persists and compounds with every case — transforms those existing assets into Intelligence Capital. It does not replace the expertise. It captures it, compounds it, and makes it permanently available to the whole organisation.

And here is the mechanism that makes the timing strategic: a competitor who deploys the same technology in eighteen months can purchase the enabling platform. But they cannot purchase eighteen months of your deliberation history. They cannot run last year's decisions retrospectively.

The gap between a first-mover and a late-mover does not close. It widens. Permanently. Time is the one input that cannot be acquired retroactively.

The Key Diagnostic Question

Apply Schreiber's three KPIs to your own organisation. They are calculable from your own data, not just from public filings. If your Scaling Quotient is negative — if growth requires proportional headcount — your AI investment is ornamental.

If your LAE trend is flat or rising despite increased automation investment, the automation is cosmetic. If your Structural Precision is deteriorating, you are buying growth.

Then ask the question that Schreiber's framework cannot answer: is your current AI investment building something that appreciates?

Not something every competitor will have by next year — but something that compounds because it captures and encodes the institutional judgment your best people carry, making it permanently available to the entire organisation, visible to regulators, and irreproducible by any competitor who starts later.

That is the question we are working through with clients across insurance, financial services and other knowledge-intensive sectors. The window to build it is open. It will not stay open indefinitely.

Simon Torrance is CEO of AI Risk and creator of the Agentic AI Accelerator. He advises leadership teams on Intelligence Capital strategy and how to implement it.