JPMorgan Spends $2 Billion a Year on AI. Here's the Layer They Haven't Built Yet.

Dispatches from the Agentic Frontier is a new regular intelligence briefing for leaders in knowledge-intensive sectors. Each dispatch translates evidence from the frontier of agentic AI — practitioner experience, investor signals, strategy research, market events — into what it means for enterprise leaders building for competitive advantage. Some dispatches are field reports from practitioners who are 12–18 months ahead. Others synthesise emerging research. All are filtered through the Intelligence Capital framework developed in The AI Your Competitors Can’t Buy.

Today we do a deep-dive analysis on JP Morgan’s AI strategy and deployments to elicit lessons for leaders across any sector.

Introduction

JPMorgan Chase has built the most impressive AI infrastructure in financial services — and it is still missing the one thing that creates durable competitive advantage. That paradox is worth understanding before you study their playbook. What they have built is extraordinary. What they have not yet built is the layer that will determine which organisations are still ahead in 2030. The evidence for both claims follows.

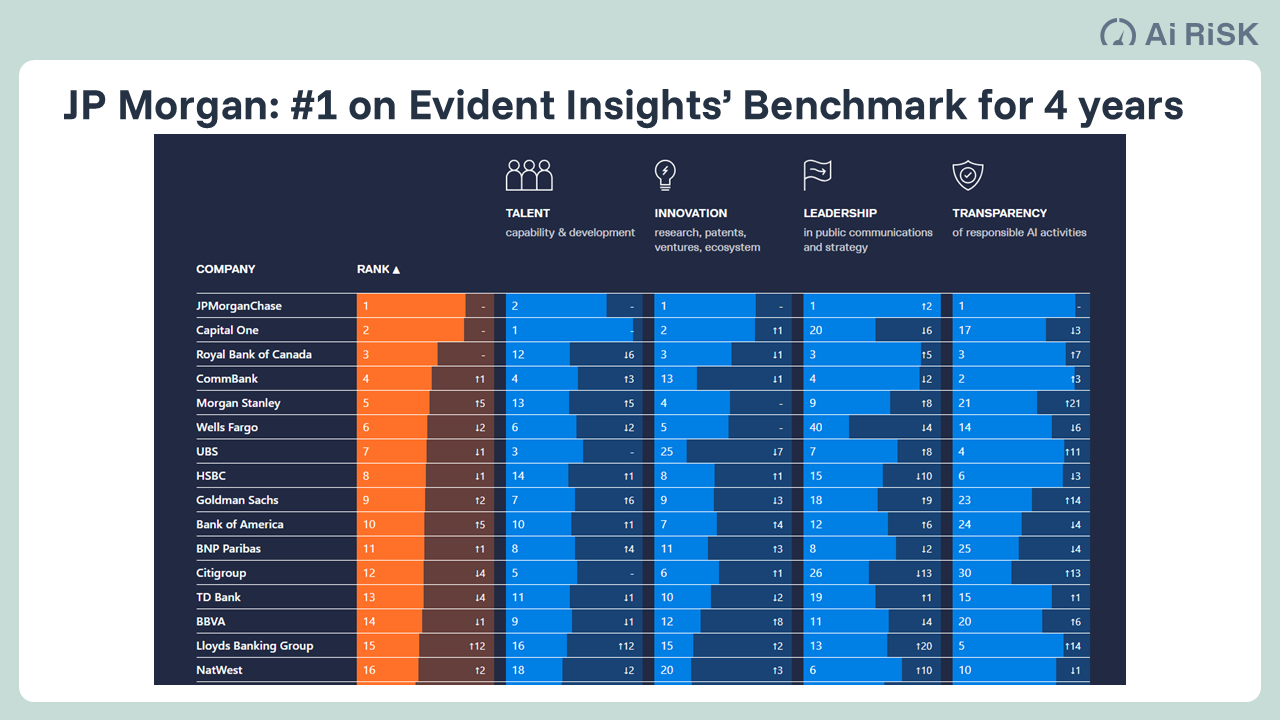

JPMorgan Chase is, by any serious measure, the most advanced AI enterprise in financial services. It has topped the Evident AI Index — the most rigorous independent benchmark of AI maturity across global banking — for four consecutive years, scoring 79.0 against an average that trails by more than twenty points.

To put that in context, for insurance leaders for example: the Evident AI Insurance Index tells a sobering story. AXA and Allianz dominate the insurance rankings, the only two insurers to place in the top five across all four pillars — Talent, Innovation, Leadership, and Transparency.

Yet even these two leaders score approximately 62 points. The insurance industry average sits at just 35.5. JPMorgan's lead over the best insurers in the world is as large as the best insurers' lead over their own industry average. The gap is not incremental. It is structural.

The scale of JPMorgan's commitment is striking, but the ratios matter more than the absolutes. Its overall technology budget is $19.8 billion, of which approximately $2 billion — roughly 10% — is now directly tagged as AI. That AI spend represents about 1–1.2% of total revenue. The bank reports approximately $2 billion in realised annual AI value, also around 1–1.2% of revenue — meaning AI investment is, in aggregate, already paying for itself. It has deployed its internal LLM Suite to 250,000 employees — not a specialist subset, but the vast majority of the workforce.

Over 100,000 use it daily: roughly one in three JPMorgan employees starts each day with an AI tool open. If those daily users each save even two hours per week, that alone represents approximately 10 million hours per year — on the order of $1 billion in time-value at typical knowledge-worker costs, sitting comfortably inside the $2 billion figure and leaving room for fraud-loss reduction and revenue uplift. These are ratios any organisation can benchmark against, regardless of budget.

This is not a pilot programme. It is an industrial rewiring of a 200-year-old institution.

And JPMorgan is one of only three banks in the world disclosing both realised and projected AI returns — most firms cannot yet measure what their AI investments are actually delivering.

Every leader running a knowledge-intensive business — in insurance, asset management, professional services, or any sector where expertise and judgment drive value — should study what JPMorgan has done. Not because you need $19.8 billion. But because the strategic choices JPMorgan made are choices available to organisations of any size. And because the gap JPMorgan has not yet closed reveals where the real competitive advantage lies.

Three Moves Most Organisations Haven't Made

JPMorgan's lead is built on governance and architectural decisions that have nothing to do with budget and everything to do with strategic seriousness.

First, they elevated AI out of IT. Jamie Dimon took AI and data out of the technology organisation and placed AI leadership directly on the Operating Committee. Teresa Heitsenrether, a business-side veteran, was appointed to lead the AI mandate — not a CTO or a data scientist, but someone who understood how the bank made money. JPMorgan remains one of only six banks in the Evident Index to have AI leadership at the executive committee level. Most organisations still treat AI as a technology initiative delegated to IT. JPMorgan treats it as a business transformation owned by the people who run revenue lines.

Second, they invested heavily in their data estate. Before deploying agents at scale, JPMorgan invested billions in cloud migration, decommissioned 2,500 legacy applications, and moved 65% of workloads to the cloud. As Dimon himself has noted, the hardest part is not the AI — it is mobilising the data.

This does not mean you must complete a multi-year data transformation before you start. Today's agentic AI platforms can connect to existing systems, work with imperfect data, and deliver value while the broader estate is modernised in parallel. But the lesson stands: organisations that treat data readiness as someone else's problem will find their AI investments amplify complexity instead of productivity. JPMorgan's advantage is not that they waited — it is that they refused to pretend the problem did not exist.

Third, they embedded AI ownership in every business line. In February 2026, the bank elevated digital head Guy Halamish to COO of the Commercial & Investment Bank with a specific remit: redesign every business unit and process to maximise AI impact. His first priority is appointing Chief Data & Analytics Officers inside each major business line — not reporting to a central technology function, but sitting beside business heads and rewriting operations with AI at the centre. This is the blueprint for federating AI ownership without losing strategic coherence.

These three moves — executive elevation, data readiness, and business-line ownership — are available to any organisation. A specialty insurer with £100 million in GWP can make them as readily as a $200 billion bank. They are choices about how you organise, not how much you spend.

The $2 Billion Paradox

Here is where the story gets interesting for strategists.

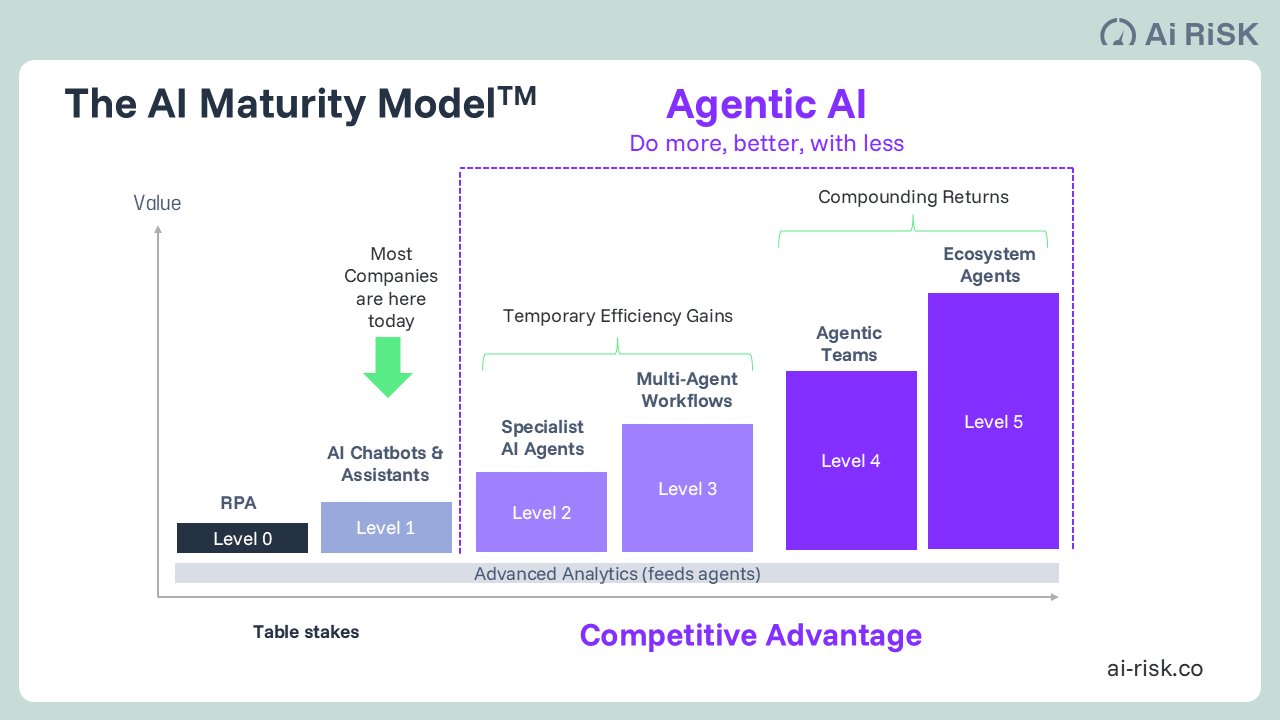

JPMorgan's ~$2 billion in realised AI value is impressive. But let’s examine what constitutes that value. The flagship use cases — COiN reviewing 12,000 commercial agreements in seconds, the Investment Bank Copilot generating pitch decks in 30 seconds, payments fraud detection, developer productivity gains — are efficiency and automation achievements. They make existing processes faster and cheaper. In our AI Maturity Model, they sit at Levels 1 through 3: AI assistants, specialist agents, and multi-agent workflow orchestration.

They are also, by definition, replicable. Goldman Sachs, Morgan Stanley, and Citi are deploying equivalent capabilities on the same underlying platforms. JPMorgan itself swaps its foundational models every eight weeks — a practice that confirms the models are commoditising. When the underlying technology is interchangeable, the efficiency advantage converges across competitors. This is what we call the Parity Problem: AI investment that buys you parity, not advantage.

JPMorgan's own leaders sense this. Chief Analytics Officer Derek Waldron acknowledges a "value gap between what the technology is capable of and the ability to fully capture that in an enterprise." CIB co-CEO Troy Rohrbaugh has signalled the strategic frontier clearly: "I'm really excited about what we potentially can do on the revenue side. That's the game-changing part of AI for our franchise."

They are articulating the transition from doing things cheaper to doing things that were previously impossible — from productivity gains to new sources of revenue and competitive advantage. The question is: what makes that advantage durable?

The Missing Layer: Intelligence Capital

Waldron describes the future as a "fully AI-connected enterprise" where every process is powered by agents. This is the right ambition. But connectivity — however sophisticated — is infrastructure. It enables value; it does not, by itself, compound it.

The compounding comes from what we call Intelligence Capital: institutional knowledge that is captured, encoded, and accumulated by AI systems with every decision the organisation makes. Unlike conventional technology investments, Intelligence Capital appreciates with use. Unlike individual expertise, it never retires, forgets, or joins a competitor.

Consider the difference. JPMorgan’s COiN system reviews contracts in seconds — an extraordinary efficiency gain. Imagine instead that every override — every time a senior partner flagged a clause the model missed — was captured with structured reasoning: why this clause matters, what precedent it sets, what the system should recognise next time.

After 10,000 contracts, the system would have encoded not just what to flag, but the accumulated judgment of every partner who ever corrected it. The 10,001st review would be qualitatively better — not because the model improved, but because institutional memory deepened. That is Intelligence Capital. The published evidence suggests COiN does not yet do this. Neither, as far as available disclosures indicate, does the IB Copilot.

The published evidence suggests JPMorgan is at the threshold of Intelligence Capital generation, but not yet across it. Their Proxy IQ system — which replaced external advisory firms for shareholder voting across $3 trillion in assets — comes closest, because it internalises market intelligence rather than merely automating a task.

AI Research lab, up until recently run by Manuela Veloso, with its work on multi-agent systems and explainability, provides the scientific foundations. But the gap between research capability and production deployment of systems that genuinely deliberate, capture reasoning, and compound institutional knowledge remains substantial — not just at JPMorgan, but across the entire industry.

There is a further risk that leaders building towards Intelligence Capital must address directly. Most agentic AI platforms store deliberation records in proprietary cloud infrastructure. Three mechanisms threaten IC ownership without deliberate architectural protection.

Acquisition risk: if your IC is stored in a vendor’s proprietary system, a platform acquisition puts years of accumulated institutional intelligence under someone else’s commercial control — the AI sector is consolidating rapidly.

Competitive leakage: standard terms of service typically permit vendors to use customer interaction data to improve models for all customers, meaning your encoded institutional patterns may sharpen the same platform for your competitors.

Migration trap: if deliberation records cannot be exported in portable formats, switching to better technology means restarting IC accumulation from zero.

The protection needs to be architectural, not contractual: define and own the output schema, store deliberation records on your own infrastructure. The vendor provides the engine. You own the intelligence it generates.

This is the critical sovereignty decision that JPMorgan’s published AI strategy does not yet address — and the one every leader building IC must resolve before they begin.

This is the opportunity for every leader reading this, regardless of organisational size.

The Lesson That Applies to Everyone

JPMorgan's infrastructure and governance moves are the floor, not the ceiling. They create the conditions for Intelligence Capital, but do not automatically generate it. The firms that will build durable advantage are those that design AI systems which don't just automate decisions but capture the reasoning behind them, retain that reasoning as institutional memory, and compound it into every subsequent decision.

This is an architectural choice, not a budget one. A 200-person insurer, for example, that builds agentic teams to capture and compound underwriting judgment — encoding why risks were accepted or declined, how claims evolved, what patterns senior underwriters recognise — will accumulate an advantage that a firm a hundred times its size cannot replicate by purchasing the same technology six months later.

The 17-point gap between the leading insurers and JPMorgan on the Evident AI Index is real. But it measures AI maturity — adoption, governance, talent, transparency. It does not measure Intelligence Capital. The race to compound institutional knowledge has barely started, and in that race, the starting positions are far closer together than the maturity indices suggest.

The window for this is not theoretical. JPMorgan's own trajectory tells us the timeline. They are shifting from research to execution, embedding AI into every revenue line, and planning for a 10% reduction in operations staff as agents take on complex multi-step tasks. Their competitors are eighteen to twenty-four months behind. In insurance, wealth management and other sectors, the gap is wider still — and so is the opportunity.

Technology can be purchased at any point. Time cannot. Intelligence Capital is the product of technology multiplied by time — and of that product, only one factor is available for sale.

The organisations that begin building Intelligence Capital now will compound an advantage that late movers cannot close — because they will lack the decision history, the institutional memory, and the reasoning architecture that only accumulate through time. First-mover advantage, in this context, is not about being first to deploy AI. It is about being first to make your AI learn.

JPMorgan has built the most impressive AI infrastructure in financial services. The question for every leader is not whether to follow their example — you should. The question is whether you will stop where they are, or build the layer they haven't built yet.

The Choice Architecture

Every leader reading this faces a version of the same choice.

Option one: follow JPMorgan’s playbook on governance, data readiness, and business-line ownership — and stop there. This buys you parity with the market leaders in two to three years, at the cost of significant investment.

Option two: follow the playbook and build the layer JPMorgan has not yet built — the deliberative, compounding, IC-generating architecture that turns every decision into a permanent organisational asset.

This builds advantage that late movers cannot close, because it is denominated in time rather than budget. The cost of not starting option two is not a missed feature. It is a gap that compounds against you, every month, from the day a competitor begins.

The organisations that recognise this window and act on it — regardless of their current AI maturity — are the ones that will still be ahead when the next capability wave arrives.

Those interested in building the architecture for option two are welcome to reach out to me.

Simon Torrance is CEO of AI Risk, an agentic AI strategy and innovation consultancy. AI Risk's Intelligence Capital framework builds on the foundational work of Professor David Shrier (Imperial College London). For more on the Agentic AI Maturity Model and the Parity Problem, see "The AI Your Competitors Can't Buy" at ai-risk.co.