Agentic Commerce: The Distribution Shift Your Board Hasn't Discussed Yet

Dispatches from the Agentic Frontier is a new regular intelligence briefing for leaders in knowledge-intensive sectors. Each dispatch translates evidence from the frontier of agentic AI — practitioner experience, investor signals, strategy research, market events — into what it means for enterprise leaders building for competitive advantage. Some dispatches are field reports from practitioners who are 12–18 months ahead. Others synthesise emerging research. All are filtered through the Intelligence Capital framework developed in The AI Your Competitors Can’t Buy.

Today we provide an updated deep-dive on Agentic Commerce. NB: Insurance is the example throughout this article. The principle applies to any knowledge-intensive sector where distribution depends on intermediaries, comparison is opaque, and a new class of autonomous buyer is about to change both. (Our original article on the topic, from October last year is here.)

Introduction

Something structural changed in insurance distribution this year. The equity markets priced it. Most boards did not discuss it.

One week in February 2026, the S&P 500 Insurance Brokers Index fell 11%. Willis Towers Watson recorded its worst single session since November 2008. Three events contributed to the move:

1. A US comparison platform called Insurify launched an insurance app inside ChatGPT

2. A Spanish insurer called Tuio did the same

3. Anthropic released new enterprise automation tools.

Three weeks later, Aviva became the first UK incumbent insurer to launch a ChatGPT app — and confirmed it intends to treat the channel as a permanent distribution route alongside brokers and Price Comparison Websites (PCWs).

Bank of America followed with a quantification: more than $15 billion in US broker commissions tied to low-complexity products face material AI disintermediation risk. This equates to roughly 10–12% of top-tier broker revenues in the US, which BofA explicitly characterised as a conservative floor.

The sell-off partially retraced in the weeks that followed: analysts called it an overreaction, and for the diversified commercial brokers it largely was. Willis Towers Watson, five months on, still trades around 10% below its pre-February level. Either way, the price action is not the point. Most boards received the sell-off as a market anomaly. It was a signal.

This article explains what the signal means — what is being built, why it changes the competitive logic of distribution, and what your organisation needs to decide before the window closes.

A new kind of buyer is being built

Every insurance transaction today is mediated by a human at some point. A consumer visits a website, uses a comparison platform, or speaks to a broker. Somewhere in that journey, a person makes a judgement. What the February launches demonstrated — in early form — is a different model.

A consumer asks an AI assistant a question about insurance. The assistant queries providers directly, compares results against the consumer's stated criteria, and returns a recommendation — without a website visit, a broker call, or a comparison platform in the conventional sense. The consumer may confirm or override, but the discovery, comparison, and routing have been done autonomously by software acting on their behalf.

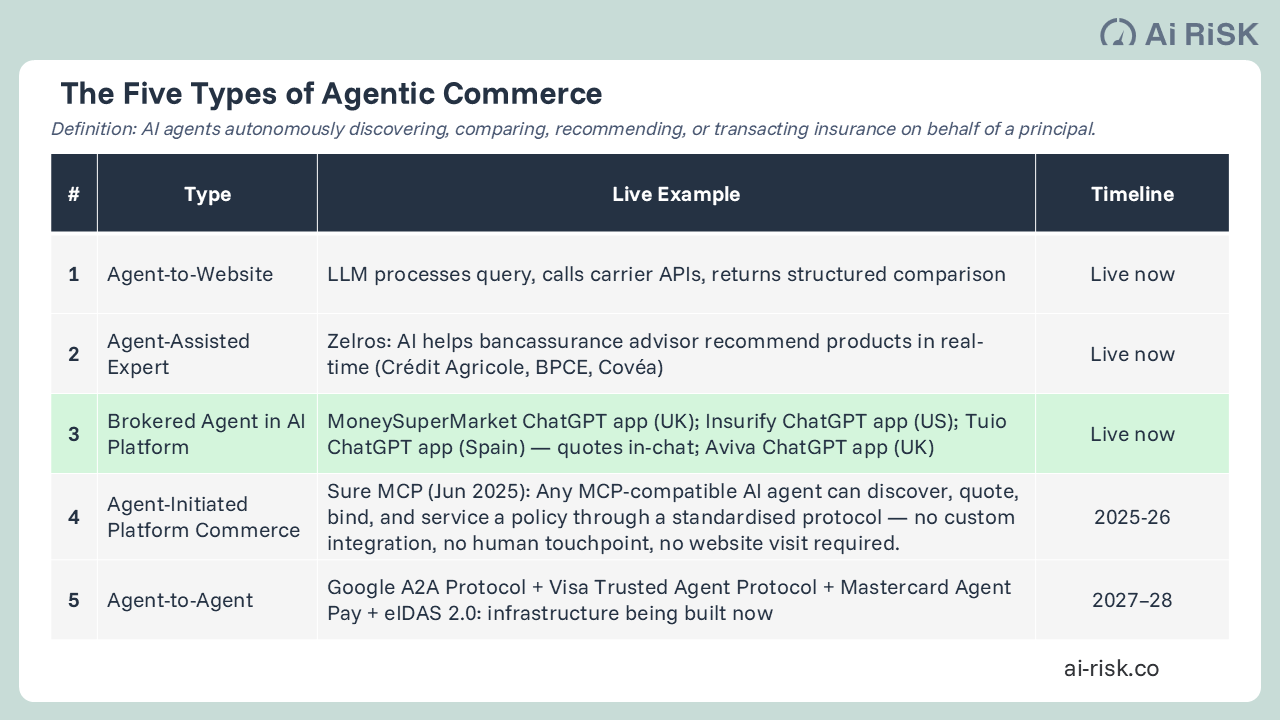

This is Agentic Commerce: AI agents autonomously discovering, comparing, recommending, or transacting on behalf of a human principal. It is not yet operating at scale. The framework below maps where it is now and where the infrastructure being built today leads.

Types 1 to 3 are live today. Types 4 and 5 are the infrastructure being assembled now. The February market reaction priced the direction of travel, not the destination. The structural positions that determine who benefits when Types 4 and 5 arrive are being claimed in 2026.

The visibility gap is already opening — and it is measurable

The first structural consequence of this shift is already quantifiable. Most carriers are losing ground without knowing it.

GEICO spends over $2 billion a year on marketing. State Farm outranks it 3:1 in AI visibility — the frequency with which a brand appears when a consumer queries an AI assistant about motor insurance. Same market. Same product category. Identical consumer intent. One brand appears. The other does not. The explanation is not brand quality or marketing spend. It is content architecture: whether products are structured in ways that AI engines can read, parse, and confidently recommend. Carriers already inside the channel are discovering why it matters: traffic referred from ChatGPT to a provider's own site converts at four times the rate of traffic arriving from traditional search.

Swiss data shows the same divergence beginning in Europe. Across major carriers in the Swiss motor market, AI visibility scores range from 50% to 67% — a 17-percentage-point spread between the most and least visible carriers competing for the same customers. European boards reading this as a US problem are misreading it. The divergence mechanism is identical. The Swiss gap will widen by the same logic that widened the American one.

Traditional advertising spend does not transfer to LLM recommendation frequency. The rules of visibility have changed. Most carriers have not changed with them.

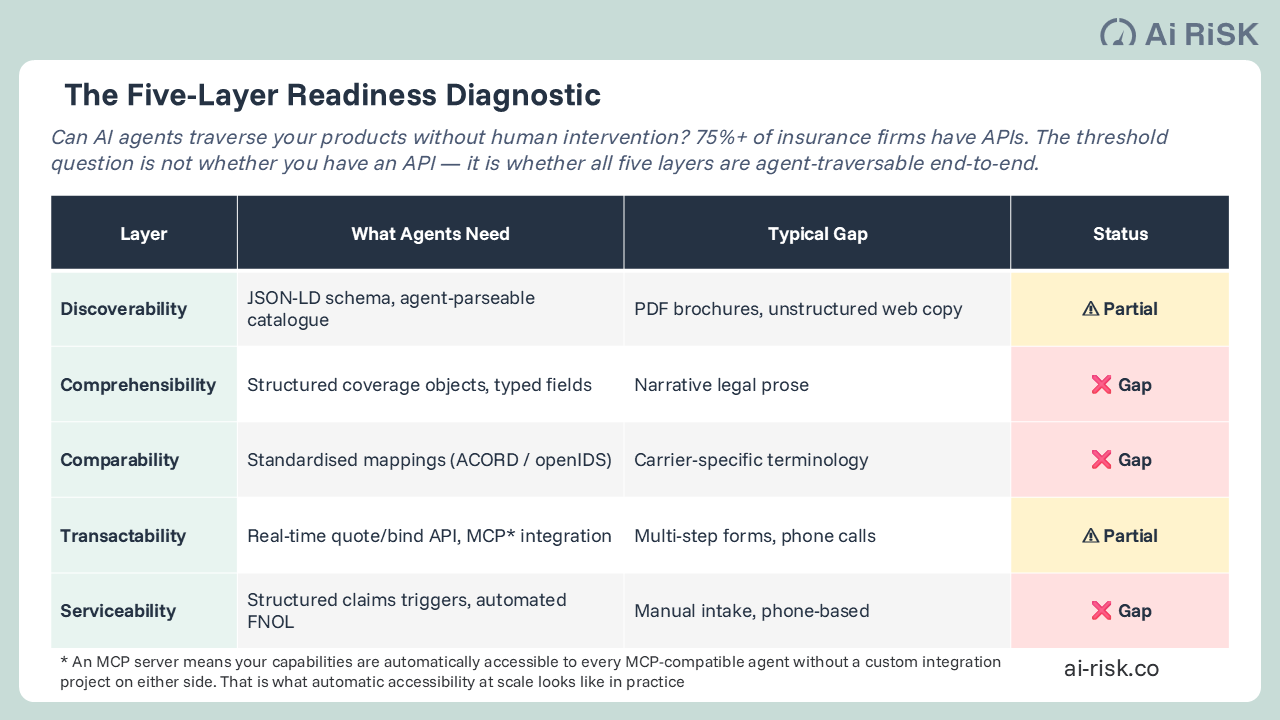

Visible is not the same as accessible

Visibility is the first threshold. Being traversable — meaning an agent that finds you can also quote you, compare you, and transact with you without human intervention — is the second. Most carriers do not clear it.

75% of insurance firms have APIs. That is not the threshold question. The threshold question is whether all five layers of your product architecture are agent-traversable end-to-end. Apply the diagnostic below honestly against your most commercially critical lines.

If the answer to any of the five questions is no, agents will route to carriers who answer yes. The agent does not call to ask for clarification. It does not return later. It moves on.

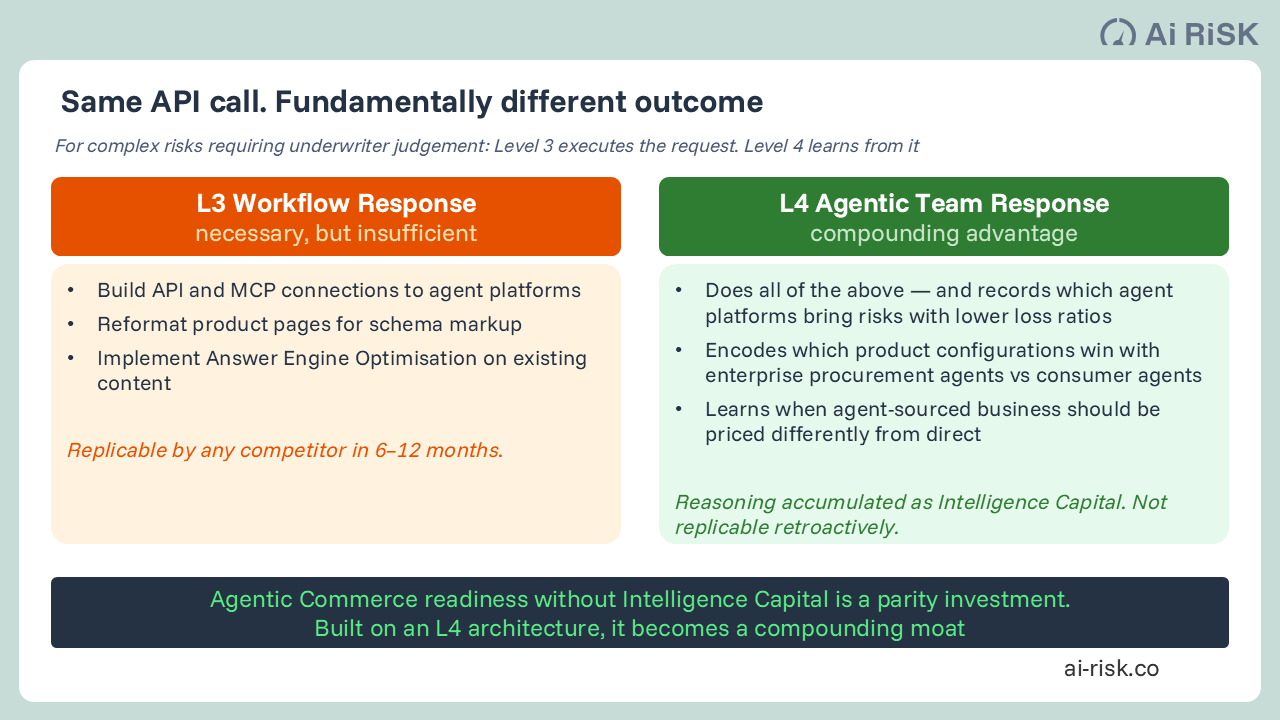

Accessibility without the deliberative layer is a parity investment

Every carrier that addresses the five layers will have done what every major consulting firm is now recommending. A competitor will replicate it in six to twelve months. That is not a competitive moat. It is the price of remaining in the game.

The deeper question is what your architecture does with the information generated by agent interactions. An agent that requests a quote and binds a policy has revealed something valuable: which platform sent it, what parameters it used, what it accepted and what it rejected. A carrier whose system captures and learns from that signal — which agent platforms bring risks with lower loss ratios, which product configurations win with enterprise buyers versus consumers — is building something that cannot be purchased retrospectively. A carrier that treats each agent interaction as a transaction rather than a data point is not.

For details of Level 3 and Level 4 and ‘Intelligence Capital’, see our article here.

The left column is replicable in six to twelve months. The right column is not replicable retroactively. One compounds. The other keeps pace.

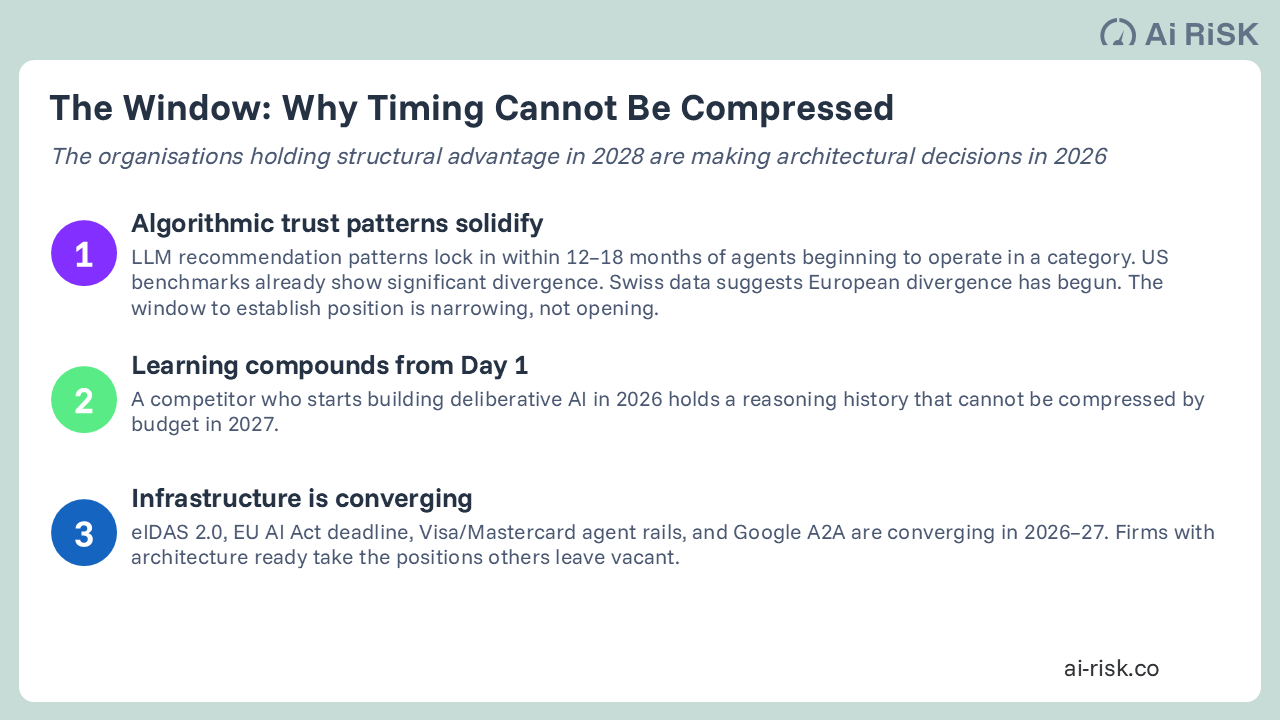

The window is narrowing, not opening

Three converging forces make 2026 the year for architectural decisions.

LLM recommendation patterns lock in within 12 to 18 months of agents beginning to operate in a category. US data shows significant divergence already established between carriers spending identically on traditional marketing. European divergence has started. A carrier that is not visible and accessible when agents begin operating at scale in its category will find those patterns already set against it.

EU AI Act high-risk compliance requirements — currently in trilogue negotiation, with a probable backstop of December 2027 — are arriving regardless of the final date. Insurers who treat the delay as permission to defer are misreading it: the accountability gap for AI agents in distribution is already being examined by regulators, and the organisations that establish technical and contractual positions before mandatory standards land will hold them. The eIDAS 2.0 European Digital Identity Wallet rollout — the cryptographic identity infrastructure that makes autonomous agent-to-agent transactions legally credible — goes live across EU member states in late 2026. That timeline is unchanged.

Three questions your board has not asked yet

The following questions are not rhetorical. Each requires work your organisation has almost certainly not done.

When your customer's AI agent comes shopping at next renewal, will your product be in the shortlist — and do you know the answer today? You cannot answer this without running an AI visibility audit across ChatGPT, Perplexity, and Google AI Overviews against your most commercially significant lines. Most carriers who have done this for the first time have found the results uncomfortable.

Of the five structural layers, which are gaps for your organisation — and in what sequence should you close them? The answer depends on your product mix, your distribution model, and where agent-sourced business will reach you first. It is not the same answer for a personal lines carrier, a specialist MGA, and a commercial broker.

Is your current AI investment building something that compounds, or something your competitors will replicate within a year? This is a board-level architecture decision. It is not a technology project.

If you want to run this diagnostic for your organisation — or to understand the full picture of what Agentic Commerce readiness requires — contact me at simon.torrance@ai-risk.co or visit ai-risk.co. You can also subscribe to Dispatches from the Agentic Frontier for the next article in this series, which covers the trust infrastructure your agents will need before they can transact autonomously.

The organisations holding structural advantage in 2028 are making these decisions now.